Everbridge (NASDAQ: EVBG) Writeup

Everbridge (NASDAQ: EVBG) Writeup

Blue Ocean, Long-Term Winner with Strengths Already Priced In

Investment Thesis

I am keeping Everbridge on my watchlist until it hits EV/Sales of ~10x. While EVBG is priced lower to its SMID-cap B2B SaaS peers despite superior fundamentals, the street is correct directionally (9 buys, 3 holds) and has captured much of the magnitude in EVBG’s long-term growth runway. Everbridge must work to achieve simultaneous growth and profitability that will increase the magnitude of its long-term earnings power, which will be driven by 1) CEM becoming a need-to-have, not just nice-to-have, service; 2) EVBG’s pioneering, deep-moated position in the CEM space; 3) its long runway of land & expand growth opportunities; and 4) margin-expanding cross/upsell opportunities to the full CEM suite. Currently, having not displayed this progress, I have a PT of $147 and a R/R of 2.0x for EVBG.

Company Overview

Everbridge is a blue-ocean CEM leader that provides end-to-end, turnkey, and scalable SaaS solutions that automate and accelerate organizations’ responses to critical events such as viral pandemics, natural disasters, cyberattacks, etc. It saves its 5.6k+ global corporate, government, and health care clients valuable time and costs by reducing IT downtime, streamlining crisis playbooks, resolving supply chain bottlenecks, etc. with its 11+ SaaS solutions (Mass Notification, IT Alerting, Public Warning, Visual Command Center, etc.). Everbridge derives 89% of its revenue from these SaaS solutions, has maintained a 37% top-line CAGR and 110+% DBNER since 2015, 70-72% gross margins since 2017, and has hovered near adj. EBITDA break-even since 2017.

Variant Views

1. EVBG leads the fragmented, fast-growing, need-to-have $40bn.+ CEM industry.

EVBG’s track record on COVID-19, cyberattacks, etc. has made CEM a need-to-have service.

EVBG has demonstrated its value proposition in crisis after crisis, but COVID-19’s omnipresence pulled forward CEM sales cycles from months/years to weeks/days.

EVBG’s turnkey (48 hr.) solutions, optionality (1 app to full suite), rapid iterations (introduced COVID Shield, contact tracing) shows inimitable value of CEM/EVBG.

Post-pandemic post-mortems and proliferation of remote work will lead firms to EVBG as the answer to, “how can we be prepared for an event like COVID?”

As a blue-ocean leader, EVBG has taken over, not part of, CEM tech & terminology.

It has also deployed $265mm in cash & stock to acquire 8 CEM peers[i] in the past 2 years.

The breadth of EVBG’s CEM suite, bolstered by its tack-on M&A, provides unparalleled optionality & comprehensive CEM coverage to customers at affordable prices.

EVBG has built tech, scale, first-mover, switching cost, regulatory, and network effect moats

Tech & Scale: EVBG’s tech (11+ apps/use cases, 7+ languages, etc.) & scale (5bn.+ in 2020 comms., 490mm.+ contact profiles, 25k data sources) are unmatched by any competitor.

First-Mover & Switching Costs: EVBG has a blue-chip client base[ii] that has shown little churn, yielded a 110+% DBNER, and has no CEM alternative apart from EVBG.

Regulatory & Network Effects: With FedRAMP, HIPAA, GDPR, etc.[ii] compliance, EVBG has exclusive govt. contracts that lead to tack-on local and corporate contracts.

2. Protected by its moats, EVBG has an uncontested, long land & expand runway.

EVBG’s services all 3 portions of its $40bn.+ TAM, which remains vastly underpenetrated.

EVBG’s 11+ apps/use cases comprehensively cover the Population Alerting ($4.8bn.), IT/IoT Alerting ($10.4bn.), and CEM ($25.9bn.) SAMs, amounting to a $40bn.+ TAM.

EVBG has only penetrated ~3% of its Population Alerting SAM and ~1% of its TAM.

EVBG is in the early innings of rapidly scaling international expansion.

EVBG has penetrated 11 EMEA/APAC countries[iv] with its Public Warning products and utilized network effects to tack-on Mass Notification, CEM deals with local clients.

An EU mandate requires members to have a population-wide alerting system by June 2022, leaving 23 countries with guaranteed demand for solutions like Public Warning.

Network effects are especially strong in nascent international markets where EVBG is running its Florida/Singapore playbook to land 1 statewide contract and expand to 100+ contracts[v].

International rev. grew 59% YoY to account for 26% of 2020 rev., while U.S. grew 28%.

3. EVBG will cross/upsell to create scale economies and ~18% adj. EBITDA margins

While it costs $1 to acquire $1 of rev. in the 1st year, it costs $0.06 to retain that $1 afterwards.

EVBG quickly amortizes its CAC by retaining initial revenue (110%+ DBNER) and increasing LTV by cross/upselling additional apps or the full CEM suite.

Strong momentum in $100k+ deals (35% YoY growth), multiproduct deals (38% YoY growth) and 66% of TTM rev. being from new products shows EVBG’s selling prowess.

Cross/upselling to CEM has driven TTM ASP to $77k+, showing how tack-on sales drive up the rev. side of unit economics while not costing much in CAC.

The average customer only subscribes to 2 EVBG apps and only 2% of clients have CEM suite, leaving significant room for EVBG to cross/upsell to.

The magnitude of the cross/upselling opportunity and its ASP/CAC tailwinds to unit economics will enable ~18-20% steady-state adj. EBITDA margins via S&M leverage.

Forest for Trees: (Attractive Unit Economics + Large TAM) * Durable Moat = LT Winner

Attractive Unit Economics: EVBG will maintain 72-75% adj. GMs while expanding adj. EBITDA margins to ~18-20% by cross/upselling and driving up LTV/CAC.

Large TAM: EVBG services its entire $41bn.+ TAM, has only penetrated 2% of it, and has recently started monetizing international markets, which are further underpenetrated.

Durable Moat: EVBG is a blue-ocean pioneer in CEM, has constructed various, deep moats, and has been rolling up CEM peers in tack-on M&A.

Valuation

My PT of $147 is derived from a probability-weighted average of 5 scenarios: 1) Blue Sky ($260, 5% weight); 2) Bull ($186, 25%); 3) Base ($152, 40%); 4) Bear ($93, 25%); and 5) Grey Sky ($66, 5%). I utilized a 10-year DCF with a 10% discount rate and 20x EV/FCF exit multiple.

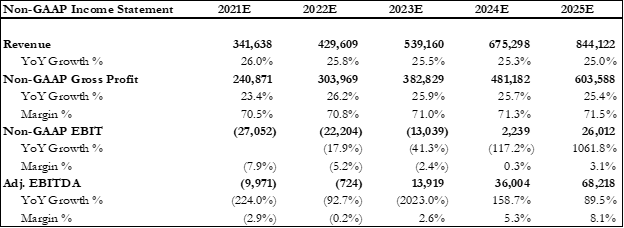

Base Case: 31.5% top-line CAGR for next 5 years, adj. EBITDA margins expand to 18%.

EVBG mgmt. executes on its LT target of mid-30% top-line growth.

Top-line driven by 500+ new annual customers, CEM upselling driving HSD ASP growth.

Margin expansion driven by steady-state GMs of 75% and scale economies driving S&M as % of rev. to 34%, mild leverage in R&D and G&A as well.

Bear Case: 27.5% top-line CAGR for next 5 years, adj. EBITDA margins expand to 12%.

Saturation in Mass Notification (50% of current rev.) & slow upselling cause deceleration.

Margins expand moderately due to steady-state GMs of 72%, slow upselling driving slow ASP growth, lower S&M leverage, while increased G&A/R&D is needed to drive growth.

Bull Case: 33% top-line CAGR for next 5 years, adj. EBITDA margins expand to 22%.

Top-line driven by 600+ new annual customers, rapid CEM upselling & avg. # of apps going to 4 apps, and new product velocity driving new use cases/end markets.

Margin expansion driven by steady-state GMs of 76%, S&M going to 31% of rev. with G&A/R&D experiencing operating leverage as well.

Blue Sky: 35% top-line CAGR for next 5 years, adj. EBITDA margins expand to 30%.

Top-line driven by 800+ new annual customers, rapid CEM upselling & avg. # of apps going to 5 apps, high use case velocity, and continued accretive M&A widening moat.

Margin expansion driven by steady-state GMs of 80%, S&M going to 30% of rev. with strong G&A/R&D leverage as well.

Grey Sky: 25.5% top-line CAGR for next 5 years, adj. EBITDA margins expand to 8%.

Mass Notification saturation, slow upselling (avg. # of apps = 3), slow CEM upgrades, increased international competition, and slow use case velocity drive sub-par rev. growth.

Steady-state GMs of 71.5%, slow cross/upselling failing to drive S&M leverage, and heavy G&A/R&D spending drive small adj. EBITDA margin expansion.

Risks & Mitigants

Post-COVID deceleration: EVBG benefitted from COVID-accelerated demand (COVID Shield, Contact Tracing) and organic growth will decelerate in a post-vaccine world.

EVBG still makes money from handling clients’ vaccination & return-to-work processes and will benefit from increased cybersecurity spending for post-COVID remote workforces.

CEM is not need-to-have: EVBG’s steady-state S&M spend will be high to maintain growth.

EVBG’s new CRO & resultant indirect sales funnel has bolstered land & expand sales strategy and will achieve stepwise cost efficiencies, especially in international markets.

Exhibits

Exhibit A (Base Case Non-GAAP Income Statement)

Exhibit B (Model Assumptions)

[i] MissionMode, NC4, Connexient, CNL, one2many, Techwan, SnapComms, Red Sky

[ii] 8 of 10 largest U.S. cities, 9 of 10 largest U.S. IBs, 47 of 50 busiest NA airports, 9 of 10 largest consulting firms, all Big 4 accounting firms, 8 of 10 largest global automakers, 9 of 10 largest U.S. health care providers, 7 of 10 largest tech companies

[iii] Anatel, Arcep, CSA, CWTA, FCC, FISMA, NIST, TRAI, DHS, CCPA, among others. No other competitors has these certifications and compliance.

[iv] Public Warning customers include Australia, Cambodia, Greece, Netherlands, Peru, Sweden, 3+ Indian states. Mass Notification and other customers include Norway, Singapore among others.

[v] EVBG scaled from 1 Florida-wide govt. customer to 400+ customers in 3 years, and from 1 Singapore-wide customer to 30+ customers in 2-3 years

Good overview, thanks! Scuttleblurb.com has a good writeup on the company too, if you want to read more on them (it requires a subscription, though).