Long Boston Omaha Corp. (NASDAQ: BOMN) Writeup

Long BOMN | Medium Conviction | Long-Term

Idea Overview

BOMN is a unique holding company with strong, silo-esque businesses in niche industries like out-of-home (OOH) billboard advertising, surety insurance, and fiber-to-the-home (FTTH) broadband. The company is underfollowed and underappreciated by sell-side coverage and investors alike, who overlook management’s solid record of deploying capital in competitively advantaged, high-ROIC[a] businesses that produce long-term, sustainable cash flows. BOMN’s intrinsic value will grow in the coming years as the company expands EBITDA margins and redeploys capital to new organic & inorganic growth opportunities – as it grows, its mispricing will correct as well.

Company Overview

BOMN was incorporated in 2015 by two co-CEOs/chairmen, Alex B. Rozek and Adam K. Peterson, to acquire a tiny public company (REO Plus). Since then, the duo has raised and redeployed capital to create BOMN as it stands today, which consists of three main business lines:

1) Link Media Outdoor, their Midwest/Southeast U.S. OOH, largely static billboard business

2) General Indemnity Group (GIG), their U.S. surety insurance underwriting & distribution business

3) Airebeam, their FTTH, fixed wireless broadband business in Arizona

as well as minority stakes in Logic Commercial Real Estate, 24th Street Asset Management, and Crescent Bank & Trust.

Link Media is BOMN’s main moneymaker (69% of FY19 rev.), has rapidly expanded in the past few years via ~$180mm of acquisitions (Tammy Lynn, Image, Waitt, Key) to ~3k billboards/5.6k ad faces, and primarily operates non-digital (digital comprises ~2% of billboards) in non-urban areas across the Midwest and Southeast U.S. GIG (31% of FY19 rev.) has expanded to all 50 states from 9 states since BOMN’s investment, and primarily underwrites commercial, small contract surety insurance. Airebeam was acquired in March 2020 and provides FTTH and fixed wireless services in Arizona between Phoenix and Tucson.

BOMN’s playbook with its businesses & acquisitions is as follows:

1) Identify locally competitive companies & assets that have inherent advantages like barriers to entry that allow them to protect and grow their intrinsic value/FCF yield over the long term

2) Acquire these companies & assets at attractive prices, verifying that the acquisition passes the hurdle of opportunity cost of investment in the other 2 main business lines & minority investments

3) Integrate acquired assets into main business lines, targeting revenue and cost synergies & efficiencies that were previously impossible or not aligned with previous management’s incentives

As of 12/31/2019, BOMN has invested $190mm+ into Link, $36mm+ into GIG, and ~$14mm into Airebeam as of March 2020. These investments have been made without any debt financings, with Rozek/Peterson rather choosing dilutive equity raises[b]. The duo has recently stated that Airebeam, as well as tack-on Link acquisitions, will be prioritized in investments moving forward. Other recent maneuvers have been to launch a $125mm SPAC (NASDAQ: YSACU) in October 2020 for larger acquisitions, deploy $20mm+ into large-cap, publicly traded securities this past fiscal year, and raise $50mm+ of capital by issuing 3mm new shares.

Variant View

As a disclaimer, my variant view on BOMN is not much of a disagreement with current consensus views on the company, as there is no consensus with such a small following. Rather my view is what the market, in time, should come around to when looking at BOMN.

1) Link and Airebeam are secure silos and BOMN’s crown jewels

Link Media – Link’s unique competitive strategy of pursuing static billboards in non-urban areas throughout the Midwest/Southeast, as well as the resilient nature of the OOH advertising industry, protect and sustainably grows the assets’ cash flow yield.

Link is the ~6th largest OOH U.S. advertiser and many of its larger peers (Lamar, Outfront, JCD, Clear Channel) pursue digital ad faces in large metros for high ROI in high traffic areas. BOMN’s strategy runs opposite to this playbook, but uniquely targets longer-term leases and less-seasonal demand. Due to their rurality, Link’s leases are over a longer term than urban and some are permanent buys. Additionally, demand for a non-urban, static billboard is demonstrably less seasonal and more stable than an urban, digital billboard – businesses in the area will buy year-round OOH ad space to support local stores, while larger businesses see digital, urban ad faces as one of many options to promote short-term/seasonal sales campaigns. Link, by acquiring assets in non-urban locations, has avoided the fierce competition in urban, digital OOH markets and has obtained longer-term leases and less seasonal demand that protect its assets during volatility (a la COVID-19)

The OOH billboard industry’s resilience amidst the market share onslaught of digital advertising is also favorable. In the backdrop of all other traditional media – newspapers, magazines, radio, TV – experiencing negative ad growth in the past 5 years, billboards have accelerated its growth from ~4% in 2015 to 4.5% & 7% in 2018 and 2019. Billboards’ resilience and resurgent growth is a product of digital’s exponential growth – with businesses looking at fewer durable channels to reach audiences, billboards are reemerging as a popular option because of limited supply and audience’s inability to skip. Additionally, regulations in the billboards industry prevent too many billboards from being built in one area, giving existing billboards a regulatory barrier to entry.

Putting this all together, Link Media is building secure silos of billboard assets in the sole, non-digital advertising industry that is accelerating in growth in the past few years. As Link continues to pursue tack-on acquisitions in non-urban U.S. areas and integrates its past acquisitions, it will only strengthen its silos and increase its earnings power potential, which I’ll discuss below.

Airebeam – Airebeam, while in a very different industry compared to Link, pursues a similar strategy of building FTTH silos in digital subscriber line (DSL) ‘deserts.’ On top of Airebeam’s growing silos, the growing demand for fiber internet is several times larger than OOH billboards.

Airebeam currently provides fixed wireless (tower to home receiver) services to 7k+ Arizonians and was acquired by BOMN due to its focus on spending its FCF on fiber services. While fiber is technologically superior to copper cables (mgmt.: if copper is 2 in. pipe, fiber is 15 mi. river), fiber still faces stiff competition with copper coaxial cables, as cable companies can bundle in phone/internet/TV plans that provide value. Therefore, Airebeam is focusing on laying down fiber in areas where the only incumbent competitor provides DSL lines, the most obsolete telephone lines. Airebeam correctly recognizes that they can obtain a first-mover advantage by being the first to providing technologically superior fiber services in areas where the only alternative is DSL. By constructing these fiber silos in DSL ‘deserts,’ Airebeam discourages other competitors from entering, competitors who also have to deal with regulations regarding over-building.

Airebeam’s fiber silos in Arizona also have a bright future ahead of them – data usage has been growing ~30% per year and there is a growing correlation between data capacity and usage. The more capacity a household is given, the more data they tend to use.

Link and Airebeam are both secure silos for BOMN and share some characteristics as the crown jewels for BOMN. They require significant upfront capital investment, as well as provide tax advantaged cash flows. While there is a shift in investor consensus these days towards asset/capital light, SaaS-like businesses, there is still an argument to be made that capital-intensive businesses have significant barriers to entry. In BOMN’s case with Link and Airebeam, the upfront capital they are putting up to acquire billboards or lay down fiber optic cables is a barrier to entry. Once BOMN erects these barriers to entry with Link and Airebeam, they enjoy tax-advantaged cash flows due to the depreciation/capex dynamics inherent with billboards and fiber. Both billboard and fiber assets tend to last longer than GAAP depreciation lifetimes and will exceed the annual maintenance capex needed for the assets. These inherent depreciation tax shields, as well as both businesses taking well to moderate levels of debt, will prove a powerful combination for BOMN moving forward.

2) Link will grow earnings power by stabilizing revenue growth and expanding EBITDA margins

Link is the strongest silo that BOMN has and will be the first to rapidly grow its earnings power via stabilizing top-line growth and expanding EBITDA margins to ~40% in the next 5 years. It will achieve both earnings drivers by consolidating its previous acquisitions and adding small, tack-on acquisitions in geographically and regulatorily attractive locations.

While 2018 was the busiest year for Link’s roll-up strategy (it did ~$140mm in 2018 M&A), management was correct when it stated that, “2019 was the most transformative year for Link to date[c],” even though Link only did ~$10mm in M&A during 2019. 2019 was indeed the most transformative year for Link because the real value-creation in its future more lies in astute branch office consolidation & precise tuck-in acquisitions and less in further large acquisitions like Tammy Lynn/Image and Waitt/Key which instantly boosted Link to be the leading player in West Virginia/Midwest, respectively.

In 2019, Link took significant strides in its management and organizational structure to achieve both aforementioned value drivers. To start off, Scott LaFoy, previously head of M&A at Link, took over for Jim McLaughlin as CEO. Having a previous head of M&A as CEO is an encouraging sign for astute tuck-in acquisitions and efficient consolidation. LaFoy, who has 35+ years of experience in billboards, quickly decentralized Link’s organizational structure and appointed 3 regional managers – Evie Conrad, Bill Lodzinski, and Rob Wamsley – for Illinois, Mid-Atlantic/West Virginia, and Wisconsin, respectively. All 3 regional managers have significant experience in billboards and come from competitors or acquired companies. With LaFoy at the helm and this newly decentralized structure, Link will be much more agile in consolidating and achieving efficiencies within the ~26 acquisitions it has previously made, as well as any future acquisitions. This agility will allow Link to get the most out of its widely dispersed billboard assets and as a result, stabilize its top-line growth over the long-term.

This agility via consolidation and decentralization is also the main operational driver behind Link expanding EBITDA margins to ~40% in the next 5 years. With Link EBITDA margins ranging from 23-26% in the past few fiscal years, management is focusing on reducing its land and overhead costs to achieve this margin expansion. While land cost as a % of revenue has increased over the past 5 FYs, overhead cost was greatly reduced in 2019 to 9.6% from 14.9% in 2018 – likely due to LaFoy’s initiatives and integration of Waitt/Key/Tammy Lynn/Image assets. As Link starts to improve land cost efficiencies and maintain this overhead cost efficiency with its consolidation playbook, it will ramp up EBITDA margin expansion. As Link stabilizes its revenue growth and expands its margins, Link will sustainably scale its earnings power considerably.

3) GIG will slowly but steadily develop into a cash cow for BOMN

Of all 3 of BOMN’s main businesses, GIG seems to be the least attractive at first glance, but there is a credible argument that it will bloom late into an important cash cow for BOMN’s deployable capital. While it is difficult to characterize GIG as a silo-like business as Link and Airebeam are, GIG is playing a smart, long-term game by being in the less competitive, low-loss vertical of surety insurance. GIG has chosen to avoid the major insurance players in the higher risk/reward profit verticals like auto, liability, homeowner’s, and worker’s comp, and scale rapidly (from 9 to 50 states) in 2 years within commercial and small contract surety insurance, which boasts loss ratios 40-50 bps. lower than the aforementioned verticals. Therefore, while GIG and its underwriting business UCS are by no means dominant leaders in surety insurance and have not built any barriers to entry to justify them being silos, they have – in usual BOMN style – chosen to operate in a lowkey, niche corner of a larger market that the leaders choose to avoid.

Operating in this secluded vertical of the insurance industry, GIG can become a cash cow for BOMN by scaling to mid-single-digit EBITDA margins, reaching BOMN’s targeted 8-12% FCF yield, and successfully investing its float. While management stated that all of Link, GIG, and Airebeam were FCF positive in 2019, COVID likely knocked GIG out of that list due to difficulties in new policy origination. As GIG scales in more lucrative markets like California, it will be able to return to being FCF positive and work on breaking even on an EBITDA basis by improving its commission/premium split. Commissions constituted 12% of GIG’s revenue to premiums’ 84% in 2019, and GIG will be able to create a small margin tailwind by employing a data-driven approach towards growing commissions – something that BOMN management has praised the new GIG CEO, Dave Herman, on. Lastly on float, GIG can be for BOMN what Geico is for Berkshire Hathaway. Buffett has extolled since 1995 about the benefits of having a large float – investable reserve of collected premiums not yet paid out – in a corporate structure like BRK/BOMN. While prudent risk management is needed for GIG or Geico’s float to be invested at a consistent underwriting profit and Rozek/Peterson do not have Buffett’s investing track record, there is a potential for GIG’s float to become its own cash cow for BOMN and the CEO duo to invest[d].

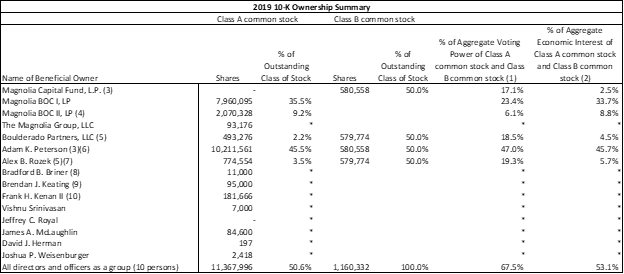

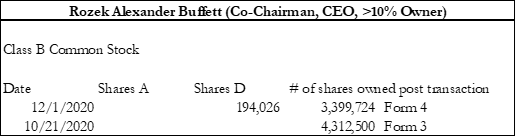

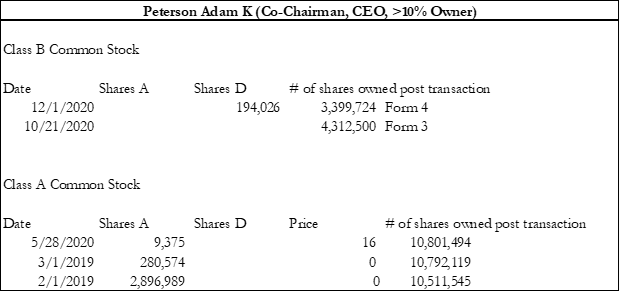

Insider Ownership

As BOMN’s success is more reliant on management discretion and incentives than many other companies I have looked at, I chose to do a deeper dive on insider ownership. Overall, all insiders, including subsidiary leaders, Rozek/Peterson, and board members, have all been buying in the last ~4 years. Rozek and Peterson remain >10% owners of BOMN and also own shares via their own investment vehicles of Boulderado and Magnolia, respectively. Additionally, all directors are required to own stock after joining the board. More information can be found in exhibit B.

Valuation

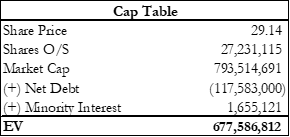

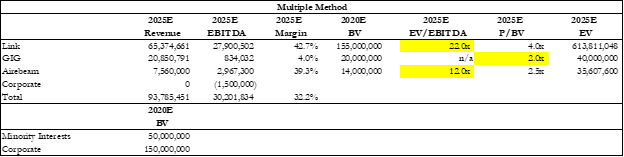

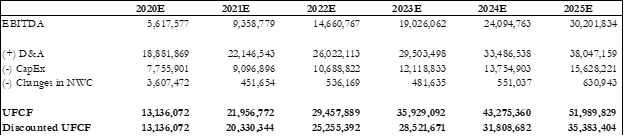

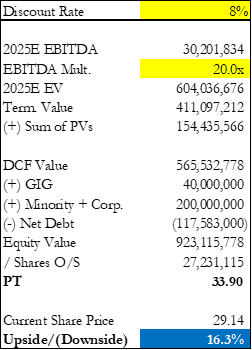

Valuation is a both an art and science, but I must add a disclaimer that it is more of an art with this BOMN pitch. BOMN grows in lumpy intervals due to its inorganic growth playbook. Since I cannot predict the timing, size, and synergies of Rozek/Peterson’s acquisitions, it is even more difficult for me to value BOMN accurately. Below in the exhibits, however, are my attempts at valuing BOMN by combining their operating assets, minority interests, and net debt. I project around 25-30% upside in the next 5 years assuming little M&A activity.

Embedded in my Link projections are assumptions that it will grow top-line at ~17% each year and expand EBITDA margins to 42.5% by 2025. Embedded in my GIG projections are assumptions that it will grow top-line at ~7% each year and achieve mid-single-digit EBITDA margins. Embedded in my Airebeam projections are assumptions that it will grow top-line ~20% each year and maintain EBITDA margins of ~38%. For valuation outputs, full assumptions, unit economics analysis, inputs, and sensitivity tables, please reference exhibits A and C-G.

Conclusion

Being long BOMN means you are long Alex Rozek, Adam Peterson, and the managers at Link, GIG, and Airebeam. While being long any other company means you are long their management, this is especially true for BOMN due to their investment process and corporate structure. Thankfully, Rozek and Peterson have built so far a great holding company full of durable, anti-fragile businesses with distinct competitive advantages and long-term earnings power. My qualitative bullishness on these businesses has led me to be long BOMN more than my valuation, which shows what BOMN can do if Rozek/Peterson reduce M&A and let these businesses stabilize and run for 5 years. I would add my confidence in their capital allocation abilities as a call option to my rough valuation and end this pitch with this bottom line – being long BOMN is a favorable, asymmetric bet due to the durability of the businesses limiting the equity’s downside, and Rozek/Peterson’s astute capital allocation providing spurts of upside.

I have taken this bet and have allocated roughly ~6% of my portfolio to this new BOMN position. I’d be happy to see other investors take this bet with me, or provide any comments/feedback.

Endnotes

[a] Management likes to use return on tangible equity capital for its OOH business

[b] BOMN recently took on $18mm of debt from Link Media (fixed for 7 years, 4.25%). All other debt at subsidiaries continues to be non-recourse to BOMN

[c] Source: 2019 Annual Letter

[d] At this point in the writeup, you have probably noticed the parallels between BOMN and BRK. It would be remiss not to throw in the fact that the B. in Alexander B. Rozek is Buffett and that Rozek is Buffett’s great grandnephew. For me, this doesn’t add value to the pitch or for my belief in Rozek’s abilities, but for others it might.

Exhibits

Exhibit A (Cap Table & Key Metrics)

Exhibit B (Insider Ownership)

Exhibit C (Valuation w/Multiples)

Exhibit D (Valuation w/DCF)

Exhibit E (Sensitivity Tables)

Exhibit F (Revenue & EBITDA Breakdown)

Exhibit G (Link Target Unit Economics)