VIA Optronics AG (NYSE: VIAO) Writeup

Long VIAO | Low Conviction | Medium Term

Idea Overview

VIAO is a German provider of enhanced display and sensor solutions to automotive, consumer electronics, and industrial/specialized applications end markets. A subsidiary of IMI, VIAO has a significant technological moat with 111 patents granted, 53 pending patents, and proprietary materials & manufacturing processes. Since its recent IPO in Sept. 2020, VIAO represents an under-the-radar opportunity for generalists and specialists alike. While suffering from high customer concentration and poor revenue visibility, VIAO has recently displayed several positive inflection points in its end markets, top-line stability, and margin trajectory that add onto its strengths of technological leadership, vertically integrated & global supply chain, customer stickiness, and high insider ownership. As a generalist, I am initiating a small starter position in VIAO based on positive inflection points that have been underappreciated by the market but holding off from a full position due to unaddressed business risks and optronics not being in my circle of competence.

Company Overview

Founded in 2005 and headquartered in Nuremburg, VIAO has progressed from being a niche player in enhanced displays to a leading provider of enhanced display solutions, touch sensors, electrode base film materials, and interactive display solutions. Over its 20+ years of engineering experience, it has amassed a suite of differentiated technologies including VIA bond plus (proprietary silicone-based bonding material) and Max VU (patented optical bonding process) alongside its aforementioned patent portfolio. Its technological leadership has enabled it to develop long-term, sticky relationships with Tier 1 suppliers and OEMs in its three main end-markets – relationships that have built it another competitive advantage of information-sharing and pre-planning for its customers’ future pipelines.

VIAO has served 60-70 customers in the last two years and major customers include BMW, Ferrari, GM and Rolls Royce in autos; Dell, HP, Lenovo, Mutto and Sharp in consumer electronics; and 3M, Dell, Emirates Airlines, GE, Honeywell, John Deere and Siemens in industrial/specialized applications. VIAO provides navigation displays, interactive display systems (supporting advanced driver assistance systems or ADAS), rear seat entertainment, etc. for its auto customers; touch/display solutions for notebooks, tablets, and monitors for its consumer electronics customers; and in-flight entertainment displays, ruggedized laptops, marine navigation systems, agricultural equipment, digital signs, interactive conference displays, and defense applications for its industrial customers. VIAO’s products are differentiated due to their superior functionality, durability, and customizability. These three traits enable their products to have better sunlight readability, usage in extreme temperatures, waterproofing, and other efficiencies in unique, challenging use cases.

Over time, VIAO has organically grown and also acquired assets/companies to become a leading one-stop-shop for its customers’ display and touch solution needs. Its partnership with Corning[i] to use its cold-formed glass technology, as well as its March 2018 acquisition of VTS – provider of metal mesh touch sensors – show how VIAO has inorganically grown its user value proposition.

VIAO’s future success, as it has articulated in its growth strategy, is incumbent on it widening its leadership as a display/touch solution one-stop-shop for its customers. By making itself indispensably valuable for its current customers, VIAO will improve top-line growth and predictability, attract new customers and new revenue from existing customers, and improve margins due to top-line stability. While it has built a formidable technological moat in a growing TAM, it must execute on this strategy to continue its positive inflection points and grow, not just protect, its earnings power and intrinsic value.

Bull View

1) VIAO, as a display/sensor one-stop-shop, will stabilize top-line growth & expand margins

VIAO has been becoming a one-stop-shop for its customers’ display/sensor needs in two ways: 1) It has made acquisitions (VTS, sensors) and partnerships (Corning, cold-formed glass) to provide a differentiated, holistic portfolio of services to its customers and 2) introduced integrated, camera-enhanced, and interactive display solutions that uniquely combine its all 3 of its offerings in an unparalleled value proposition. These two strategies increase VIAO’s indispensability to its customers as it increasingly offers customizable, valuable solutions that cannot be easily obtained from competitors or without significant switching costs.

Each step that VIAO takes to become an irreplaceable one-stop-shop comes with a step-wise increase in its customer stickiness, which will reward it with stabilized top-line growth in-turn. VIAO’s customers are also incentivized to choose VIAO as a sole supplier due to its vertically integrated supply chain. By designing & manufacturing most of its subassemblies, VIAO enjoys unique flexibility to provide its customers a wide, customizable range of products that affords customers production/cost efficiencies of their own. This provision of cost efficiencies via supply chain integration is a competitive advantage that is matched only by a few competitors.

Another positive externality of VIAO’s move towards becoming an exclusive one-stop-shop is its increasingly deep collaborations with its OEM/Tier 1 supplier customers. VIAO’s strong value proposition has incentivized these customers to allow VIAO in early on their R&D processes in hopes that VIAO can collaborate to provide customizable value-adds to products in their pipeline. By getting its foot in the door early, VIAO not only enjoys better customer loyalty and more revenue visibility, but erects more barriers to entry for competitors that have to match VIAO’s product offerings without this deep level of collaboration. VIAO has built this collaboration competitive advantage in all 3 of its main end-markets, with its collaborations on interactive displays for car interiors & camera-assisted ADAS-supporting displays for its auto OEMs as its crown jewels.

The earnings impact from VIAO’s emerging status as a one-stop-shop is stabilization of top-line growth and expanded margins. As a reliable one-stop-shop, VIAO will reduce its dependence on product wins/revenue conversions and maintain steady streams of revenue. Additionally, its deep collaborations with OEMs will enable it to anticipate future demand and mitigate the chances of a boom-and-bust earnings structure. By stabilizing its top-line growth and earning more revenue predictability, VIAO also earns itself cost efficiencies via supply-chain visibility that will expand its margins. VIAO will also expand margins by upselling higher-margin, customized products like interactive displays to its customers, which will be elaborated upon in the 2nd bull view.

2) VIAO will expand margins by shifting to auto/industrial end markets and a unique product mix

Apart from expanding margins via supply chain efficiencies, VIAO will also improve its unit economics by shifting to the favorable auto and industrial/specialized end markets and improving its product mix by upselling higher-margin interactive and touch-sensor integrated displays.

Since 2017, VIAO’s display solutions segment has been shifting from consumer electronics to industrial/specialized applications as its largest end-market. Currently, management expects industrial/specialized to continue being its largest end-market, followed by autos and consumer electronics. This shift in end-market mix has brought with it a GM tailwind, as products sold to autos and industrial/specialized customers tend to have a price premium due to their superior functionality, durability, and customizability. Additionally, VIAO’s touch sensor segment currently has the same end-market mix as 2017-era display solutions with consumer electronics as the largest. While management expects the same transition to occur in touch sensors as it occurred in display solutions, it expects consumer electronics to remain the largest end-market for the next 2 years.

VIAO’s margin expansion opportunity via end-market transitions in its display and sensor segments is significant and management does have a track record to show for it. This end-market transition driver also carries an associated benefit of longer revenue contracts, as auto & industrial/specialized customers tend to have longer production cycles than consumer electronics customers.

Adding onto this margin expansion opportunity is VIAO’s ability and intention to upsell its customers higher-spec, higher-margin solutions such as integrated displays. Such solutions combine many of VIAO’s core competencies such as enhanced displays, touch sensors, camera tech (from IMI), and cold-formed glass (via Corning partnership). VIAO’s unit economics significantly benefit from the sales of these higher-margin solutions, and an increase in sales mix of these integrated solutions will be a long-term margin tailwind for this company. In addition to these solutions bringing a margin tailwind, they will also expand VIAO’s addressable market and widen its moat over competitors.

Bear View

1) VIAO’s one-stop-shop status will not improve its revenue concentration problem

VIAO’s 5 largest customers accounted for 89%, 82.5%, and 73.7% of 2017, 2018, and 2019 revenue, respectively. VIAO’s largest customer accounted for 40.9%, 28.4%, and 30.5% of revenue in the same years, respectively. In the first half of 2020, VIAO’s five largest customers (Dell, Pegatron, Toppan, AU Optronics and TOA) combined to account for 80.3% of revenue and represented 40.6%, 17.9%, 14.3%, 4.1% and 3.4% of revenue, respectively.

VIAO’s high revenue concentration risk manifested itself in 2019 when revenue dipped 20% YoY. The drop in revenue was due primarily to 3 large customers – Dell, AU Optronics, and Mutto – whose lower than anticipated revenue caused a 24.6% YoY drop in the display segment revenue. Each customer had a unique explanation for its drop in revenue – Dell cited delays in production due to shortage in Intel microprocessors, Mutto chose to do optical bonding in-house pursuant to a license granted by VIAO, and AU Optronics itself had a drop in revenue from one of its customers, which led to it sending less revenue to VIAO. Despite each event being unusual, it is impossible for VIAO to prevent any of these events from occurring in the future, which is a significant problem in the backdrop of revenue concentration (from top 5 customers) only decreasing to 73.7% as of 2019.

This revenue concentration problem does not improve if VIAO can execute on its strategy of becoming an exclusive one-stop-shop for its existing customers. The only solution is to attract new customers, which becomes a market share problem for VIAO over the limited pool of OEMs/Tier 1 supplier customers. While VIAO should be able to attract new customers and reduce concentration as it increasingly becomes a one-stop-shop, it must accelerate its de-concentration to reduce the risks of lumpy decreases in revenue.

2) VIAO’s earnings power is overly dependent on its customers, who wield problematic leverage

VIAO’s 2019 revenue rut was caused by over-concentration, but exposed the more significant long-term risk of its buyers’ high bargaining power/leverage. VIAO seems to be at the middle of a series of dominoes which it is at the mercy of at the first sign of trouble. Even if its customers are very loyal, a Dell or Mutto can experience a revenue drop of its own and be forced to send fewer checks to VIAO, which bears no fault or control over the situation. Additionally, VIAO’s customers have in the past wielded their bargaining power to receive reduced prices, pricing/quality/delivery commitments, and other contingencies that pose headwinds to VIAO’s gross margins and competitive positioning. To add onto the pain, VIAO is also exposed to liability risk in some of its customer arrangements.

To sum up, VIAO currently is in a position where it must pursue and anticipate its customers’ production cycles and demand conditions to earn product wins and convert them into revenue in a timely fashion. This revenue is subject to potential drawdowns that it has no control over, and in some cases its customers have no control over either. Even if it secures purchase orders, its customers may demand price/delivery/etc. contingencies that hurt VIAO’s unit economics. In order to mitigate this problematic cycle, VIAO again must de-concentrate its revenue streams and execute its one-stop-shop strategy to increase its bargaining power over existing & new customers.

Insider Ownership

As VIAO has both a strong bull and bear case by my standards, it was essential for insiders to have a high ownership stake in the company for me to initiate a position. Thankfully, that is exactly what I found. Jürgen Eichner is the next largest shareholder of VIAO after IMI (48%), owning 14% of shares. Additionally, Eichner and the CFO Jürgen’s annual bonus is tied to profit measures. Eichner has a lot of skin in the game, and his high % of ownership aligns his incentives with shareholders. As a side note, Corning owns 6% of VIAO. VIAO’s ownership summary can be seen in exhibit F.

Valuation

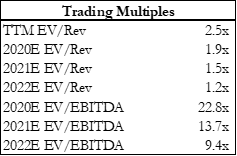

Value-minded investors (rare in these 2021 markets…) should be conscious of cost basis when initiating a VIAO position, as well as pay close attention to gross/EBIT margins due to their impact on future upside. Sensitivity analysis shows variance is disproportionately positively skewed, but prudent maintenance due diligence is needed to verify that theses, whether bull, bear, or hold, are coming to fruition. In my view, investors should look to buy VIAO shares at $15 or below, as aggressive margin expansion & revenue growth expectations are needed to create meaningful upside from prices above $15. I have initiated my position below this level and believe that my shares will appreciate at an LDD IRR over the next 2-3 years given realistic assumptions on top-line, COGS, and operating expenses. My base case being above current consensus also gives me conviction in VIAO being currently mispriced. Nonetheless, as VIAO continues to report its next few quarters, I expect to gain better visibility for my model inputs. My valuation assumptions and outputs can be seen in exhibits A-E.

Conclusion

As I did my due diligence on VIAO and expressed my thoughts via my model and writeup, I was torn over whether to initiate a small starter position or pass. To me, the strength of the qualitative bull/bear view on VIAO is in a 60/40 split and the valuation shows me that it just passes my hurdle rate. I do like the business but also do not want to let the sunk cost of my hours of research influence me into buying it instead of passing on it. Ultimately, I realized that I was missing much more to VIAO by just looking at the business model and unit economics/earnings power.

Ahead in VIAO’s path lay concrete catalysts of increased sell-side coverage/better screening, disclosure of new, large customers (Tesla is suspected to be the ‘leading US-based electric vehicle company’ that VIAO shipped prototypes to in 3Q2020), and expansion to new verticals. At the end of the day, VIAO is a leader in a growing market of displays/touch-enabled technology and its moat ensures that it will be a durable player for years to come. While it will hit bumps in the road like any other company, its superior competitive positioning will likely support it taking a larger chunk of future market value. By tunnel-visioning on the granular aspects of the bull/bear debate and the valuation drivers, I was missing the larger picture of VIAO’s industry tailwinds.

By putting all my thoughts together, I decided to initiate a small starter position (~2% of my PA) in VIAO. As always, I welcome any thoughts or feedback on my work on the company. If you have any detailed questions, message me privately and I will share my full notes and model. Cheers, until the next writeup.

Appendix

Exhibit A (Cap Table, Trading Multiples)

Exhibit B (Variance Table)

Exhibit C (EV/Rev Multiple Valuation, used as exercise)

Exhibit D (DCF)

Exhibit E (Sensitivity Analysis)

Exhibit F (Insider Ownership Summary)

[i] Corning also invested in VIAO via a private placement after the IPO of VIAO ADSs. Corning bought 1,403,505 ADSs.

Nice writeup! Is there a way to contact you?